For any queries, email us at [email protected]

For any queries, email us at [email protected]

For any queries, email us at

[email protected]

The best kind of trades are those where the outcome is known with 100% certainty. You might wonder whether such trades exist. The short answer is yes, they do. These opportunities to make risk-free money are known as arbitrage opportunities and are the holy grail for all traders. Most crypto traders are familiar with arbitrage across spot exchanges, i.e. buy and sell a crypto on two exchanges with different prices. However, arbitraging across bitcoin futures exchanges is something that is not very well understood. Futures – Futures arbitrage across crypto derivatives exchanges is what I aim to demystify in this article. Read on!

What's in this post

Arbitrage is an opportunity to make riskless profit by taking advantage of the differences in price of a crypto asset across two or more exchanges. In traditional financial markets, such price discrepancies tend to be quite small and short lived because there are large number of traders (e.g. high-frequency trading, HFT firms) that are actively tracking and trading arbitrage opportunities.

In contrast, cryptocurrency arbitrage opportunities are relatively abundant and are easy to exploit. There are two main reasons for existence of these arbitrage opportunities: (a) trading activity/ liquidity is quite fragmented because there are a plethora of exchanges with several access restrictions in place and (b) trading is dominated by retail participants and the arbitrage hunting algorithmic traders are yet conquer crypto trading.

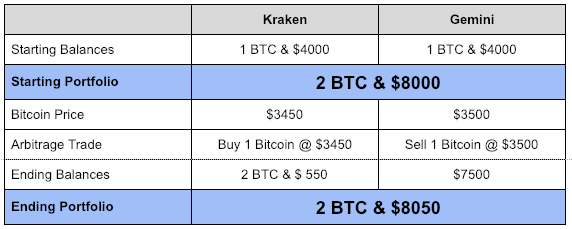

This is also known as direct arbitrage is the most basic type of arbitrage trade. Here, a trader notices discrepancy in price of bitcoin across two crypto exchanges. Obviously, the price of bitcoin should theoretically be same at all exchanges and hence such a price discrepancy presents an arb opportunity. To capture the arbitrage, the trader will buy bitcoins at the exchange where bitcoin price is lower and simultaneously sell the same quantity of bitcoins at the other exchange (where bitcoin price is higher). These two trades result in the trader pocketing the price difference as profit. The table below illustrates how such an arbitrage works in practice.

The trader has balanced of bitcoin and USD on both exchanges and is able to capture the $50 price discrepancy between bitcoin prices on Kraken and Gemini.

From the discussion above, it is clear that the basis for the spot-spot arbitrage is one fundamental truth: a bitcoin is a bitcoin and hence its price should be the same everywhere. Can the same be said about bitcoin futures contracts? Answering this question requires some understanding of futures contracts.

A futures contract is derivative contract in which two parties agree to buy/ sell an asset at a pre-specified price and future date. A futures contract is actually comprised of an expansive set of specifications that govern the behaviour and nature of the contract across all scenarios. You can see a real life example of this on the contract specifications page of Delta Exchange.

If two futures contracts trading on two different exchanges have the exact same specifications, then theoretically they should have the same price. In practice, contract specifications across exchanges are unlikely to be identical. However, arbitrage between two futures contracts is still possible if the following three conditions are met:

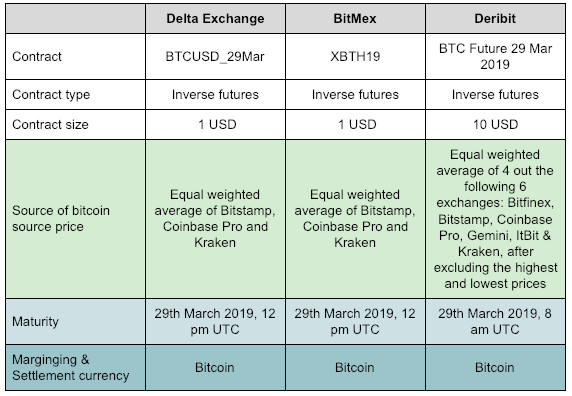

Let’s compare the March bitcoin futures listed on the three exchanges across the three dimensions mentioned above and see if there is a possibility to run future-futures arbitrage strategies on these exchanges.

The specs of bitcoin futures contracts on Delta and BitMex are identical. On Deribit, the contract is defined slightly differently, but the differences are small enough and can be ignored for practical purposes. So, futures-futures arbitrage is indeed feasible between any two of the three exchange.

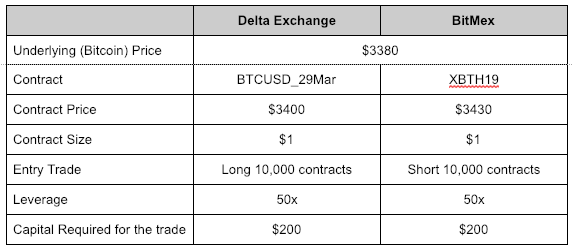

Let’s consider a situation where BTCUSD_29Mar on Delta is trading at $3400 and its counterpart, XBTH19 on BitMex is trading at $3410. Since, the bitcoin futures on Delta is cheaper than on BitMex, the arbitrage trade would be go to long BTCUSD_20Mar on Delta and short the same quantity of XBTH19 on BitMex. Goes without saying that you’d need to pre-deposit bitcoins in your Delta and BitMex wallets to be able to make this trade. Let us know analyse the possible outcomes of this trade.

In this scenario, the prices of the two contracts converge after some time. Typically, this convergence happens within minutes.

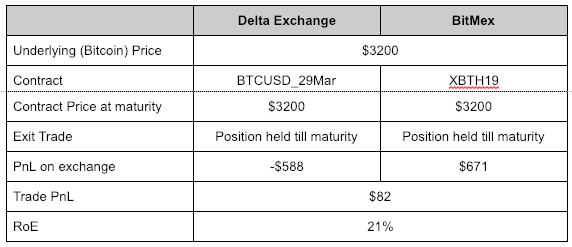

In this scenario, the convergence doesn’t happen till there is trading going on in the futures contracts. Here the contract maturity will come to our rescue. Recall that at contract maturity, the price of a futures contract converges to the price of the underlying. Since, both BTCUSD_29Mar of Delta XBTH19 of BitMex have the same underlying, the prices of these two contracts will be the same at contract maturity.

There are a few things here that are worthing noting here:

Once a trader has entered a futures-futures arbitrage trade at the right prices, the key risk for a trader is not being able to keep his positions on both exchanges open. An open futures position could be closed forcefully by the exchange in two scenarios:

Both liquidation and auto-deleveraging are risks for the arbitrage trade because capturing arb profits (without assuming any risk) requires the trader to have equal and opposite positions on the two exchanges. If a trader is running futures-futures arbitrage strategy, she will need to monitor her positions and manage liquidation and auto-deleveraging risks.

Crypto markets are open 24/7/365. Arbitrage opportunities can come up at any time. To make it easy for traders to track and capitalise upon such trading opportunities, we have created a system that continuously monitors prices of bitcoin futures (as well as futures on altcoins) and sends alerts in real-time whenever an arbitrage opportunity comes up. These alerts are sent on Telegram and Twitter. Please join this telegram channel and follow this twitter account to get these alerts.

Given the competitive nature of cryptocurrency trading, arbitrage opportunities are keenly observed by a multitude of traders. As many traders nearly simultaneously act to capture arbitrage opportunities, the price discrepancies start to get corrected. We have observed that in the case of bitcoin futures-futures arbitrage, the price discrepancies typically last for a few minutes. So, if a trader has balances on each of Delta, BitMex and Deribit, she has time to place arbitrage trades. However, time is certainly of the essence and the delay between arbitrage becoming available and trade execution can lead to slippage. Therefore, it is best to run arbitrage strategies programmatically.

What if you sold an ETH straddle daily for six months (June 2023 to Jan 2024)? How would your capital have grown? What levels of risk would you have been exposed to? Description of Trading Strategy Underlying Asset: ETHEREUM (ETH) Strategy Type: Daily ATM Straddle Selling (A straddle simultaneously

Trade Bitcoin Futures with Stablecoin – Bitcoin USDC Quantos Bitcoin futures traded on major crypto exchanges such as BitMEX, DeriBit and on Delta Exchange require traders to maintain margin & earn P/L in Bitcoin terms. This means that your margin is exposed to risk in prices of Bitcoin du

Going short bitcoin can enable you to profit from decline in price of bitcoin or any other cryptocurrency. There are a variety of ways in which short exposure to bitcoin is possible. These include bitcoin futures, margin trading, CFDs and options. Considering the available liquidity, leverage and ma

In this blog we unravel margin trading and futures trading and break them down to simple concepts. It is meant to form a basic understanding of how leverage works and how it can be a huge asset for traders if used responsibly. The post is meant to serve as a primer for margin trading & futures t

Stay Connected With News, Updates And More